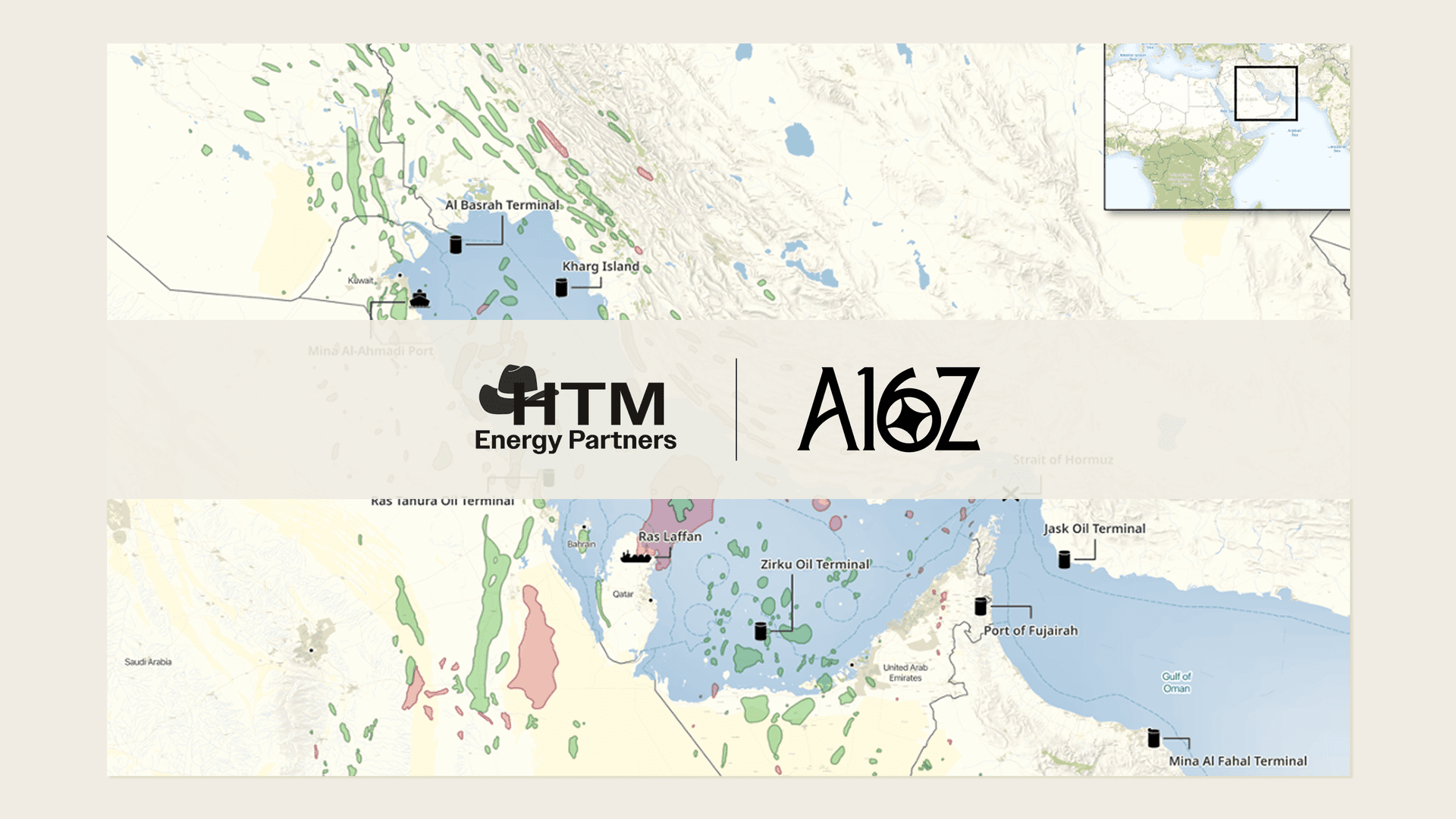

The Strait of Hormuz, often likened to the US-east-1 of global energy trade, is now a critical global dependency with no failover. Its prolonged closure triggers cascading consequences far beyond gasoline prices, impacting food, freight, fertilizer, petrochemicals, power, manufacturing, and ultimately, political stability.

This mirrors tech's understanding of hidden centralization; a single point of failure can cripple a seemingly distributed system. Today, global energy markets face a similar vulnerability with the Strait of Hormuz.

The Middle East's geological advantage, with massive conventional oil fields like Ghawar producing significantly more than US shale wells, made it a historically prudent energy source. This low-cost production, state-owned and highly profitable, fueled regional economies.

However, the world's reliance on this region, while economically logical in a vacuum, has become a strategic oversight. The Middle East's unique geology, offering massive conventional oil accumulations that are simple to produce, has resulted in the world's most prolific oil fields.

The region's strategic imperative shifted with the rise of US shale production. To maintain economic relevance and profit from their hydrocarbon advantage, Gulf states focused on monetizing the entire molecular value chain, moving beyond raw crude.

This downstream integration, accelerated by the 1998 oil price crash and fueled by growing Asian demand, saw the Gulf states become vital suppliers of plastics feedstock, LNG, LPG, and condensate. This created deep, hard-to-break dependencies across Asia, from cooking fuel in India to power generation in Taiwan.

Like proprietary software stacks, the Persian Gulf's deliberate build-out of critical industrial processes has made its energy and materials output irreplaceable. Asia's ~38 mmbbls/d of refining capacity is not easily rebuilt.

The Strait Jacket

The Persian Gulf is now paralyzed, stranding a significant share of the world's energy supply. Approximately 15% or more of global production across key hydrocarbon and commodity categories is unable to reach its intended buyers. This includes not just crude oil, but also industrial gases, refined fuels, metals, and fertilizers.

Pricing at the margin means the loss of Middle Eastern supply is catastrophic, impacting physical markets for condensates and petrochemicals, and financially curbing global pricing. Asian countries, reliant on just-in-time delivery, are feeling the immediate pain.

Substitutes are scarce and distant, with shipments from the Americas taking months. A prolonged closure would lead to unsolvable global energy shortages.

Visibility into Strait activity is deteriorating, with vessels switching off transponders. Recent estimates show a 95% reduction in normal daily transit levels, even accounting for alternative routes and shadow fleets.

Saudi Arabia's East-West pipeline is operating at capacity, but still leaves millions of barrels of crude and product exports impaired. The UAE and Iraq have rerouted some supply, but Kuwait, Bahrain, and Qatar are largely trapped.

The infrastructure impacted represents 15-20% of global liquids supply, with 10% unable to be exported by any other means.

Insulated, Not Immune

The West, as net energy exporters, has not yet felt the full impact. However, North America's export position and distance offer only a temporary buffer.

Prompt cargos from the US Gulf Coast are already heading to Asia, and China's restriction on product exports is leaving buyers scrambling.

Strategic Petroleum Reserve releases provide only short-term relief, not a solution to the fundamental problem of the Strait of Hormuz closure impact.

Financial Manipulation or Physical Desperation?

Dislocations in crude oil pricing, such as the wide spread between WTI and Brent, are not indicative of manipulation but of extreme physical market dislocation and delivery timing issues.

The cost of freight has surged, making prompt barrels in accessible locations significantly more valuable.

Omani crude's premium to WTI highlights the desperation for barrels that can reach Asian refiners quickly, underscoring the physical reality of the blockade.

Disruption Disbelief

Unlike the Russia-Ukraine conflict, where supply rerouting largely mitigated losses, the current situation presents an observable, physical stoppage. An estimated 10-15 mmbbls/d of oil is missing from the global market.

The hostile third party blocking the Strait creates a fundamentally different supply shock than when Russia simply found new buyers.

While alternative export terminals are maximizing output, the Strait's impairment remains critical. The market's relative calm, despite this massive disruption to the Persian Gulf energy trade, belies the severity of the situation.

Glut-be-Gone

The expected global oil surplus for 2026 has evaporated. Strategic stockpiles are being drawn down, and collective releases from IEA member countries cover only about a month of lost Gulf supply.

Combined with available Iranian and Russian oil, the world has backfilled approximately 45 days of lost production. However, full field-level shut-ins in the Gulf have become unavoidable, with cumulative production losses already exceeding those seen in the initial weeks of the Ukraine conflict.

Even in an optimistic scenario of immediate resumption, significant expected production for 2026 will not materialize, fundamentally altering global energy inventories.